TL;DR

- $920 psf ppr — the cheapest of the 8 Lentor parcels sold since 2021

- haio's estimated breakeven ≈$1,582 psf vs the $2,050–$2,350 psf indicative band

- 499 family-sized units: zero 1-bedders, carpark ~0.81 per unit

- Kingsford's realized record: 213 matched Normanton Park pairs, 95% profitable

- Interactive stack view + affordability widget to run your own numbers

Lentor Gardens Residences previews on 4 July with 499 units, not a single one-bedroom apartment — and the cheapest of the eight government parcels sold since the Lentor estate's first tender in 2021. Those two facts are the whole story. Kingsford paid $920 per square foot per plot ratio for the site, $358 psf ppr less than the parcel the government awarded eleven months later, and then designed every one of its 499 units for people who plan to live in them. What follows is haio's full read of the project — the land economics, the developer's record, the unit mix, the floor-plan fine print, and the six neighbours whose 2,715 caveats already frame what 4 July has to beat.

Preview timing per the project's marketing. Project and unit figures are from the project's architect briefing (P&T Consultants for Kingsford, May 2026), on file with haio; the project is not yet in haio's launch-tracking database, so briefing figures will be re-verified against URA records as they land. Land-tender figures: URA Government Land Sales tender records. Transaction prices: URA caveat data, haio transaction records, as at 12 June 2026.

1. Project details

| Detail | Figure |

|---|---|

| Project | Lentor Gardens Residences |

| Developer | Kingsford Lentor Pte Ltd (site tendered by Kingsford Huray Development Pte Ltd) |

| Architect | P&T Consultants Pte Ltd |

| Location | Lentor Gardens, Ang Mo Kio planning area — District 26 |

| Tenure | 99-year leasehold |

| Site area | 20,639.4 sqm (~222,160 sqft) |

| Total units | 499 |

| Blocks | 3 blocks × 16 storeys + 1 block × 8 storeys + 3 two-storey strata terrace houses |

| Commercial | est. 129 sqm of shops at level 1 + an Early Childhood Development Centre on site |

| Parking | 402 carpark lots + 4 accessible + 84 bicycle lots |

| Carpark ratio | ~0.81 per unit — 406 car lots (402 + 4 accessible) ÷ 499 units |

| Expected vacant possession | 31 December 2030 |

| Preview / launch | 4 July 2026 |

Source: project architect briefing (P&T Consultants, May 2026). Tendering entity: URA tender records. District: haio property records.

The reality checks that belong next to that table:

- You're buying 2030. Expected vacant possession is 31 December 2030.

- The parks are future parks. The project directly borders the future Hillock Park, Linear Park and Green Link, and the developer claims 100% of units face park or pool.

- Walking distance to Lentor MRT (Thomson–East Coast Line). The enclave's retail and supermarket sit at the station under Lentor Modern.

- Schools in the vicinity, per the briefing: Anderson Primary, Mayflower Primary, CHIJ St Nicholas Girls', Presbyterian High, Anderson Serangoon Junior College and Nanyang Polytechnic.

- The headline facilities are water: a 75m skyline pool and a 50m lap pool — the longest pool footprint in Lentor, per the developer — plus a full tennis court, gym, clubhouse and sky terraces on the 9th storey of the three tall blocks.

Source: project architect briefing (P&T Consultants, May 2026).

2. Land price: the cheapest parcel in the estate — and what it says about the launch price

Start where every land story should: the award. URA tender records show the Lentor Gardens site went to Kingsford Huray Development Pte Ltd on 9 April 2025 for $429,230,000 against a maximum GFA of 43,343 sqm — $920 psf ppr ($9,903 psm of GFA), with just 2 bidders at the table. To see this award against every other parcel the government has sold in the estate:

Government Land Tenders — psf ppr

Lentor Gardens (this site): $920 psf ppr — about 28% below the richest award on this list.

Land: URA tender-result releases (psf ppr = award price ÷ max GFA) · breakeven: haio itemized estimate, $380 psf central construction (§2 method) · launch median: first 3 months of new-sale caveats, haio transaction records

Eight parcels in five years, and the chart reads one way: $920 psf ppr is the lowest land rate in the estate's history — below even the two soft-market 2023 awards, and $358 below the parcel awarded eleven months later. The developer's briefing claims a "$350+ psf lower land cost than the latest Lentor parcel"; for once, a marketing claim checks out exactly against URA records.

The breakeven ladder. What does $920 of land in every buildable square foot mean for the launch price? These are haio estimates, not the developer's books — built cost by cost, with every assumption stated on its step and below the chart:

Breakeven Ladder (haio estimates)

URA award: $429,230,000 ÷ 43,343 m² maximum GFA.

$350–$413 psf: the 3Q2025 quantity-surveyor band intersected with current development-cost references; central $380.

6% of construction cost (typical range 5–7%).

3.5% of land plus construction (typical range 2–5%).

3% of gross development value (typical range 2–4%).

6.5% of total costs (typical range 5–8%).

4% of total development costs (typical range 3–5%).

Central estimate; the band spans $1,544–$1,624 across the construction range.

If the developer prices in a margin

5% developer margin on the central breakeven estimate.

10% developer margin on the central breakeven estimate.

15% developer margin on the central breakeven estimate.

haio estimates — illustrative developer economics built from the stated assumptions, not the developer's books. Percentage costs that scale with the selling price (marketing, legal/statutory, contingency) are solved simultaneously with the breakeven. Actual breakeven moves with design efficiency, financing terms and launch timing.

Assumptions (haio estimates): land at $920 psf ppr (URA award, above); construction at $350–$413 psf, central $380 — the 3Q2025 quantity-surveyor band for an above-average-standard condominium ($293–$413 psf) intersected with the $350–$500 psf range in current development-cost references; professional fees at 6% of construction (range 5–7%); financing and interest at 3.5% of land plus construction (range 2–5%); marketing and sales at 3% of gross development value (range 2–4%); legal and statutory soft costs at 6.5% of total costs (range 5–8%); contingency at 4% of total development costs (range 3–5%). The cost shares that scale with the selling price are solved simultaneously with the breakeven — T = [L + C + 0.06C + 0.035(L + C)] ÷ (1 − 0.03 − 0.065 − 0.04) — giving ≈$1,582 psf central (range $1,544–$1,624 across the construction band); saleable area assumed roughly equal to maximum GFA. Margin rungs are applied to the central estimate. Actual breakeven moves with design efficiency, financing terms and launch timing.

Two comparisons give the ladder its meaning. First, run the same arithmetic on the March 2026 Lentor Central parcel ($1,278 psf ppr) and its central breakeven lands around $2,010 psf — the estate's next launch starts roughly $430 psf deeper in the hole than this one. Second, set the ladder against what Lentor new launches actually transact at: the six selling projects' launch medians run $2,103–$2,258 psf (§8). Even the +15% rung (≈$1,819 psf) sits roughly $280–440 psf below that band. That gap is not a promise of a cheap launch — it is the developer's option: Kingsford can undercut every neighbour and still clear a healthy margin, or price with the enclave and keep the spread. Which way it goes is the single most important number on 4 July.

3. Developer track record: Kingsford prices to move

Kingsford Development (Singapore, Australia, China) lists six Singapore projects in its briefing. Rather than compare launch-year medians with today's medians — different units, different markets — haio matched actual buy→sell pairs: the same unit, bought and later sold in haio's transaction records, with each pair's outcome annualized — CAGR = (exit price ÷ entry price)^(365 ÷ days held) − 1 — so a quick flip and a long hold read on the same scale. Every matchable pair, project by project:

| Project | Matched pairs | Median CAGR | Profitable | Unprofitable |

|---|---|---|---|---|

| Kingsford Hillview Peak | 35 | +0.4%/yr | 23 | 12 |

| Kingsford Waterbay | 50 | +2.1%/yr | 46 | 3 |

| Normanton Park | 213 | +3.4%/yr | 202 | 11 |

| The Hill @ one-north | none — no resales yet · 99.3% sold (developer sales, Apr 2026) | — | — | — |

| Chuan Park | none — no resales yet · 93.8% sold (developer sales, Apr 2026) | — | — | — |

| One Marina Gardens | none — no resales yet · 66.1% sold (developer sales, Apr 2026) | — | — | — |

Source: haio transactions data (URA caveat records), as at 12 June 2026 — consecutive transactions of the same unit form one buy→sell pair; each pair's CAGR is (sale price ÷ purchase price)^(365 ÷ days held) − 1, gross of stamp duties, interest and transaction costs, and the table shows the median across each project's pairs. One Waterbay pair exited exactly at its entry price (counted in neither column). Caveat records stopped carrying unit numbers after 2021, so the Hillview Peak and Waterbay pairs cover exits up to May 2021. Normanton Park row: haio market data (resolved unit records; URA's public caveats mask unit numbers after May 2021) — 213 pairs, 178 sub-sales and 35 resales, exits June 2024 to May 2026, median 4.0-year hold. The three projects still in their sales periods have no resale history yet; their rows show % sold instead, from URA's monthly developer-sales survey (units sold by developers ÷ total units, as at end-April 2026, the latest published month): The Hill @ one-north 141 ÷ 142, Chuan Park 859 ÷ 916, One Marina Gardens 619 ÷ 937. Developer sales lead caveat lodgements by weeks-to-months, which is why these figures run ahead of caveat counts. Unit counts: haio project records, matching the developer's briefing.

Three honest reads from those pairs:

All three completed projects let their buyers out in profit — one emphatically, one comfortably, one barely. Normanton Park is the emphatic record: 202 of 213 matched exits made money, median +3.4% a year over a median 4.0-year hold, and just 11 sellers went backwards. Kingsford Waterbay is the comfortable one: 46 of 50 matched exits made money, median +2.1% a year over a median 4.6-year hold. Kingsford Hillview Peak is the cautionary one: 23 of 35 exits profitable at a median of just +0.4% a year over a median 5.0-year hold — and 12 of the 35 sold below their purchase price. Gross of costs, a third of Hillview Peak's early leavers went backwards.

The windows face opposite ways — read the medians accordingly. The Hillview Peak and Waterbay pairs are early exits, by construction: their buyers bought off Kingsford's launch pricing (2013–2017) and left within roughly one market cycle, before the 2021–2025 run-up. That those medians are positive even on that unflattering window is the encouraging part of the record. Normanton Park's pairs are the mirror image — bought at the 2021 launch, sold into the run-up — so its fatter median says as much about the market it exited into as about the project. Neither window says anything about what patient holders made.

Kingsford moves volume early. Normanton Park lodged 1,411 new-sale caveats in its first year — 76% of 1,862 units. Chuan Park did 675 of 916 (74%) in year one. That is a developer with a pattern of pricing to sell, not pricing to sit — directly relevant to how aggressive 4 July might be. At 499 mostly two-bedroom units, Lentor Gardens Residences looks far more like the Normanton/Chuan playbook than The Hill @ one-north's slower, pricier 142 units.

First-year caveat counts: haio transactions data, as at 12 June 2026. Unit counts: project architect briefing (developer's own track-record page).

4. Unit mix: half the project is two-bedders — and the spec says owner-occupier, not investor

| Type | Units | Share of project | Size range |

|---|---|---|---|

| 2-bedroom | 252 | 50.5% | 646–732 sqft |

| 3-bedroom | 139 | 27.9% | 872–1,012 sqft |

| 4-bedroom | 105 | 21.0% | 1,184–1,356 sqft |

| Strata terrace | 3 | 0.6% | 1,496 sqft |

Source: project architect briefing (P&T Consultants, May 2026). Total: 499 units. The single largest unit family is the 2-bedroom-plus-study series at 732 sqft — 147 units across its variants.

What's missing is the investor product. All six earlier Lentor projects transacted units between 452 and 538 sqft at their smallest; Lentor Gardens Residences starts at 646. There is no studio tier to soak up entry-level demand — which makes the returns history of family-sized units the bet that matters:

Bedroom Performance by District

Repeat-sales method · matched buy→sell pairs of the same condo unit, held >5years · bedroom counts from haio's unit catalogue · buckets under 30 pairs show no bar

Neighbouring-project smallest-unit figures: URA caveat data, haio transaction records, as at 12 June 2026.

The mix is only half the story — the layouts confirm who it's for. Every two-bedder is a dumbbell layout with two bathrooms; the three- and four-bedders run wide-frontage family formats; and above them sit just three strata terrace houses. One risk worth naming now rather than on launch day: 252 broadly similar two-bedders is a lot of one product for an outside-central-region enclave to absorb. Kingsford is betting on depth of owner-occupier demand, not breadth of investor demand.

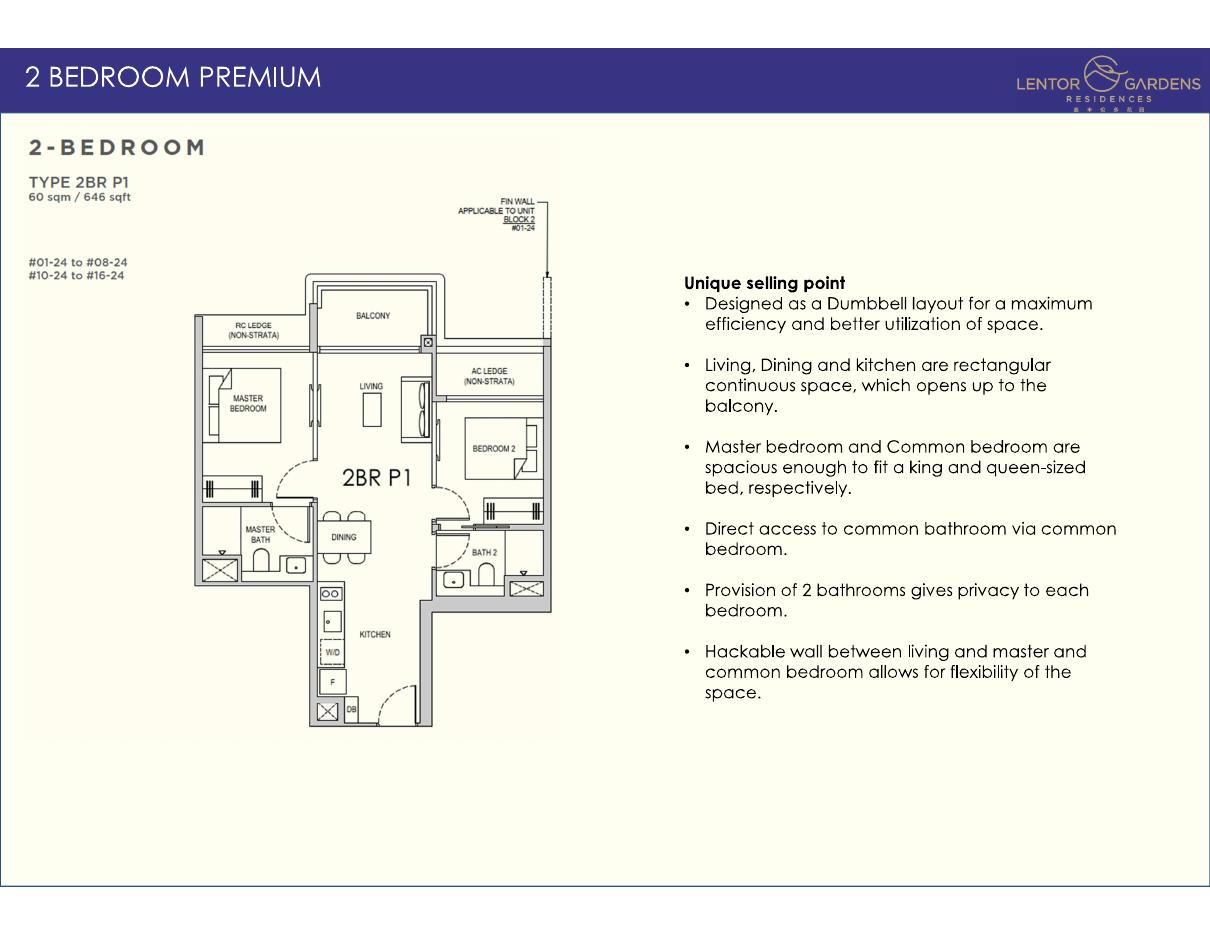

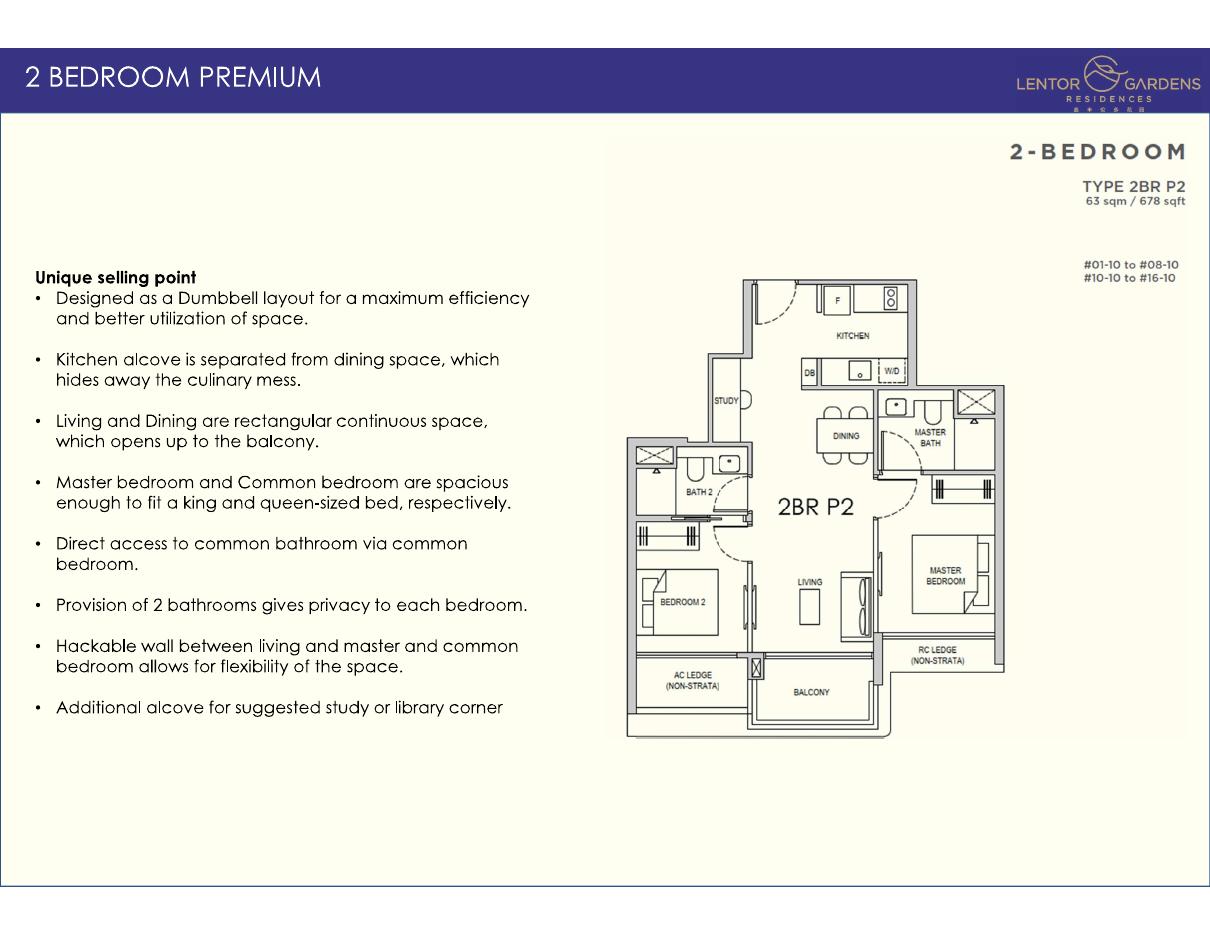

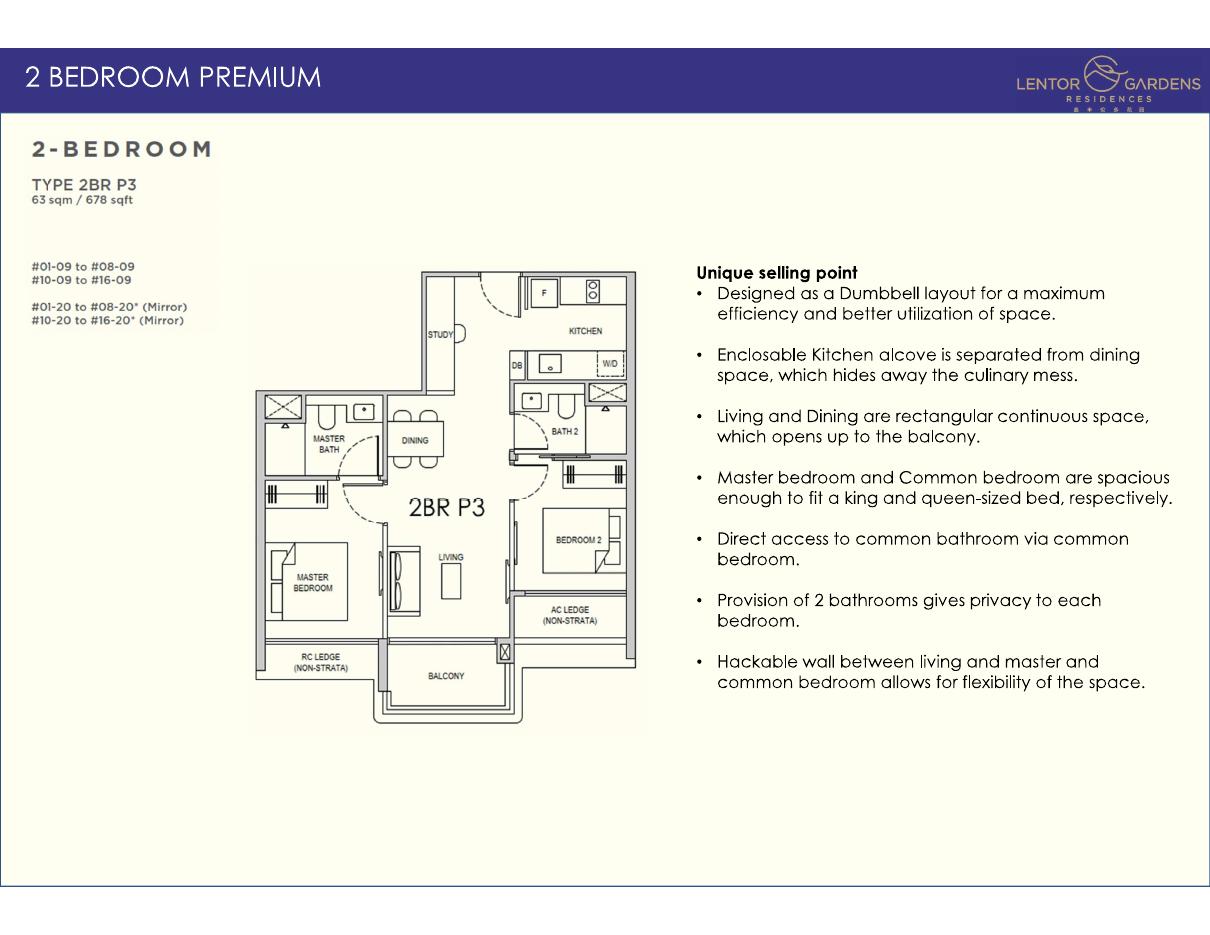

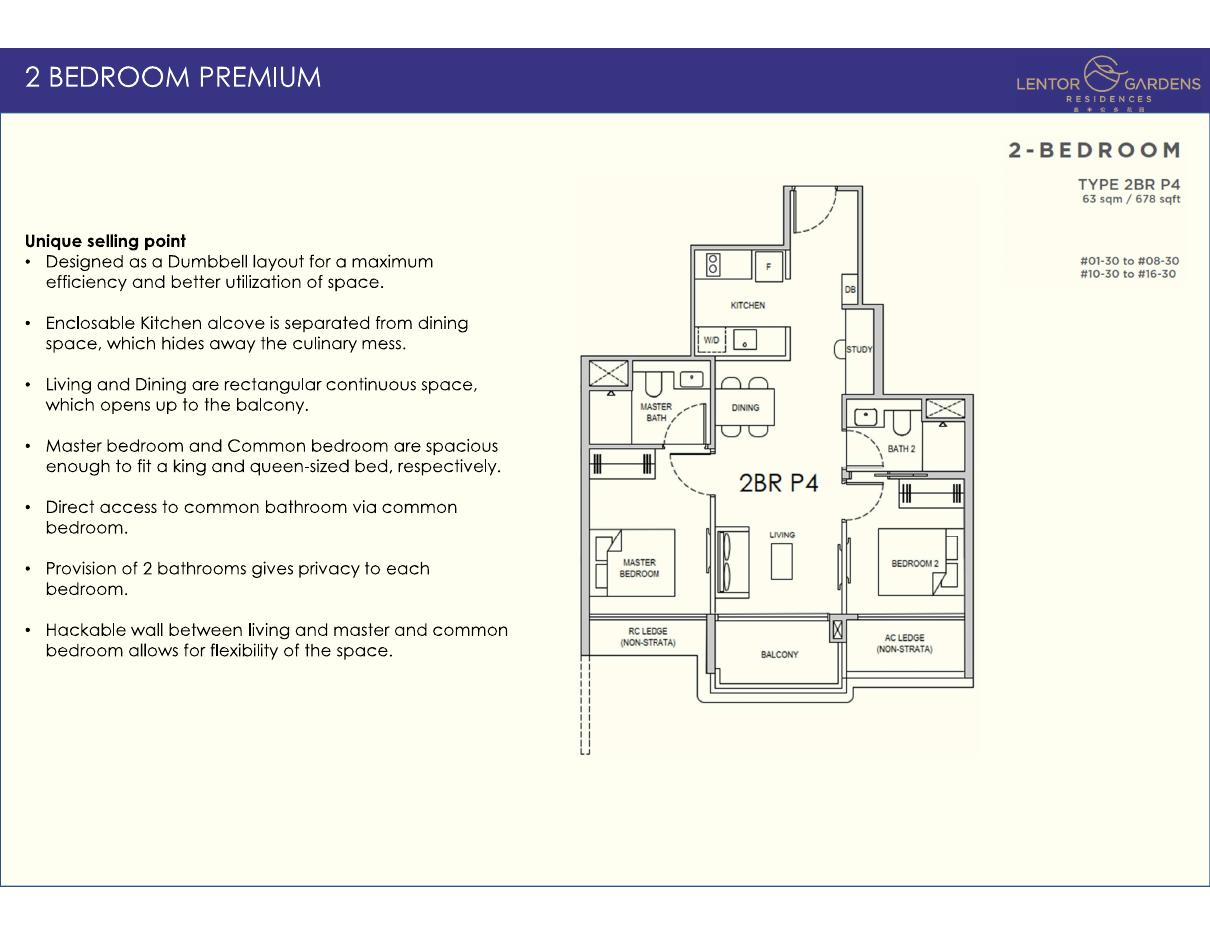

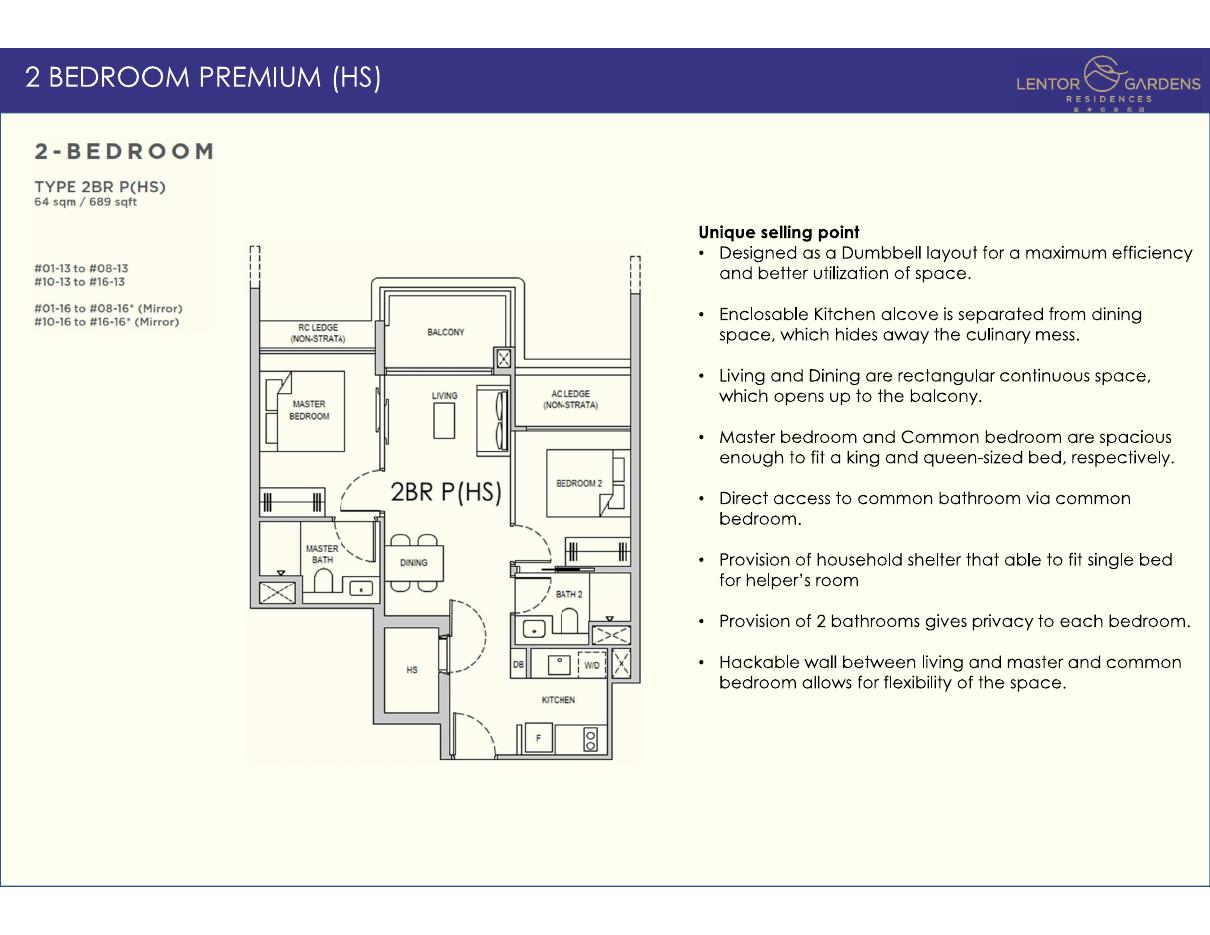

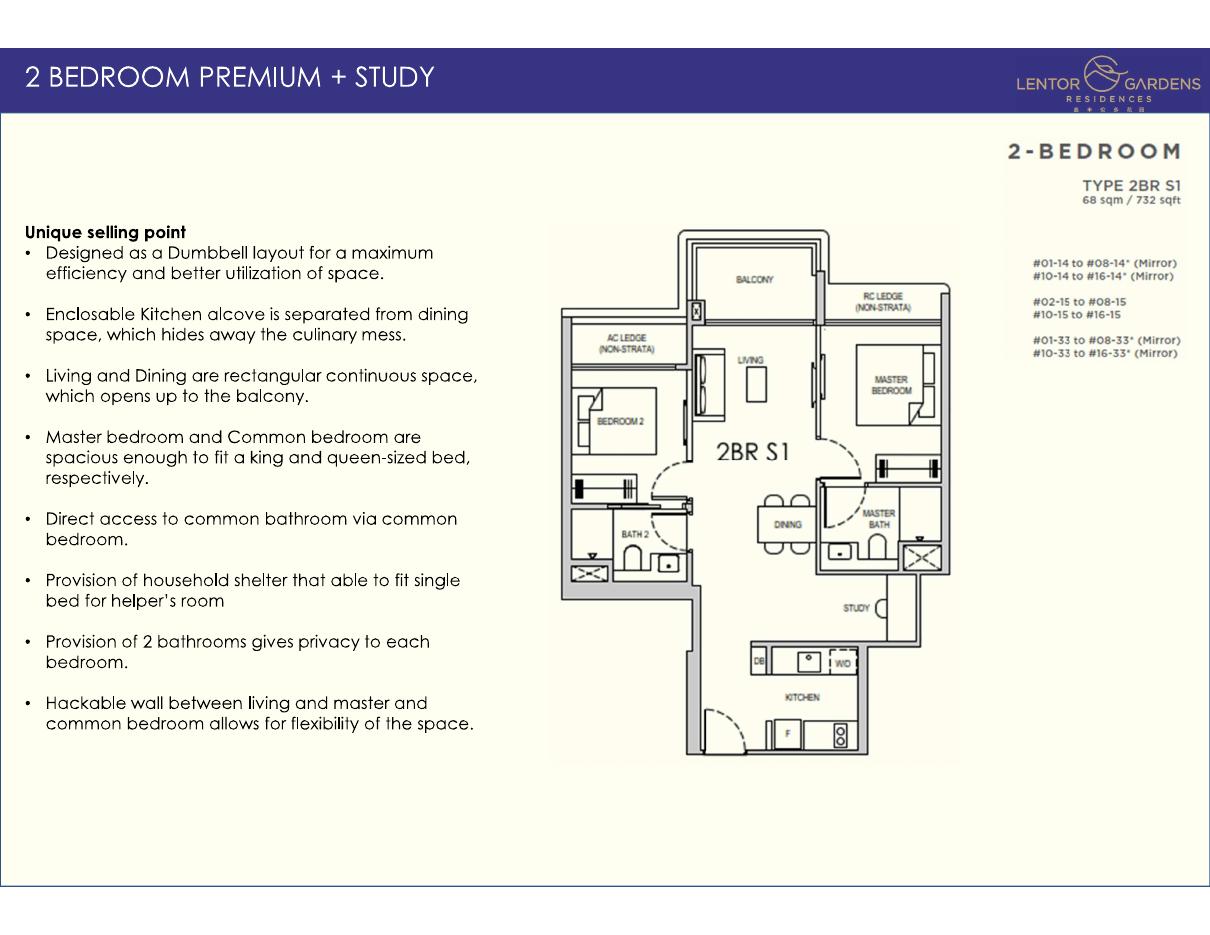

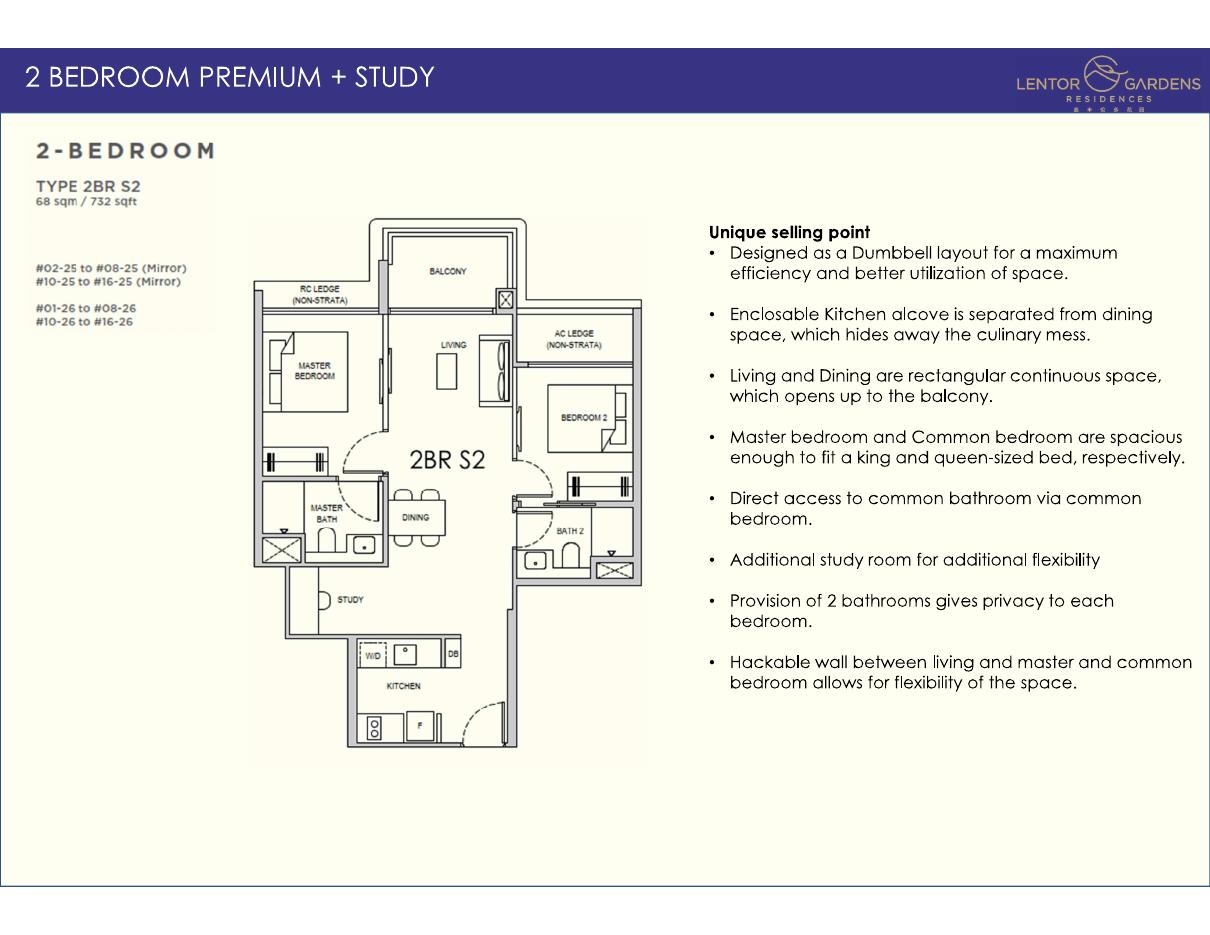

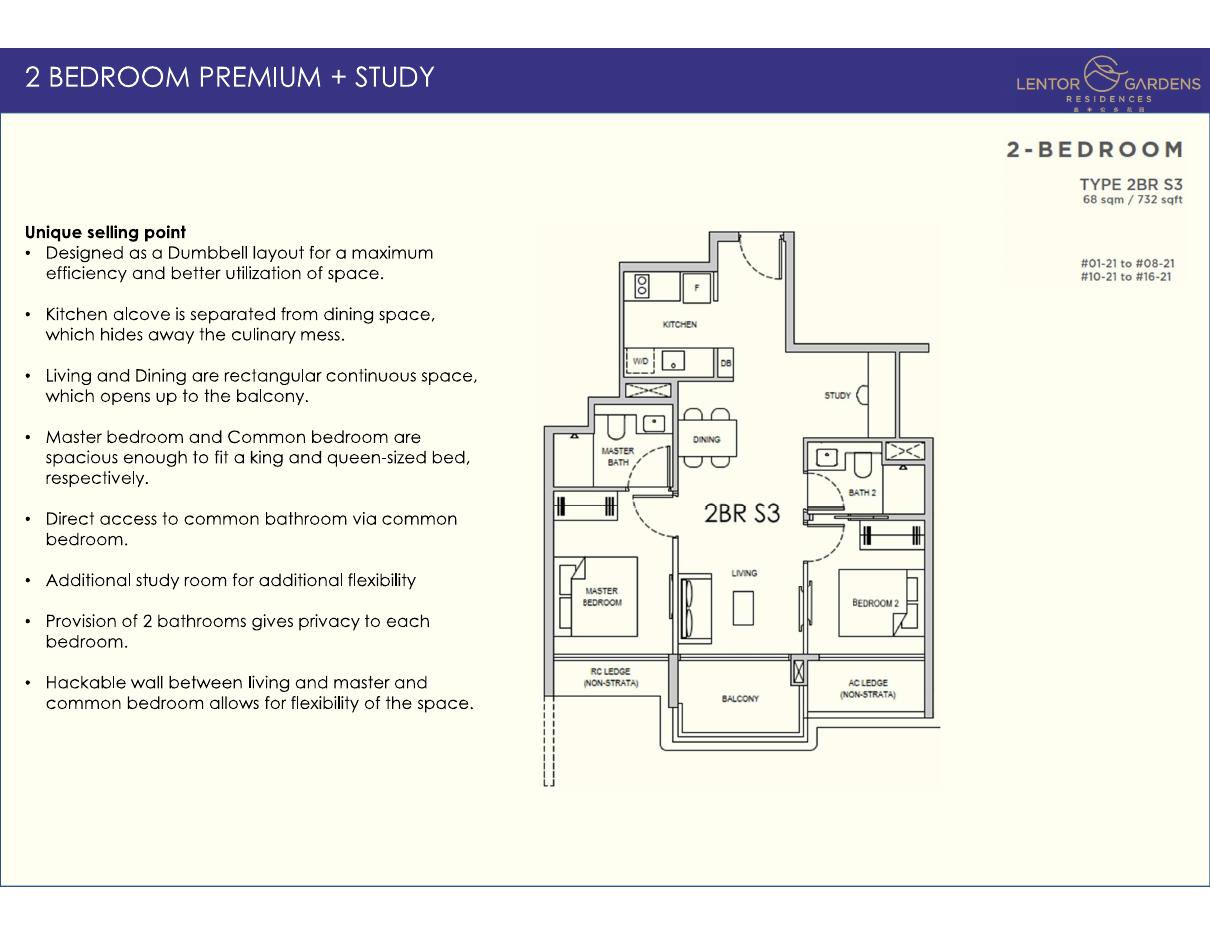

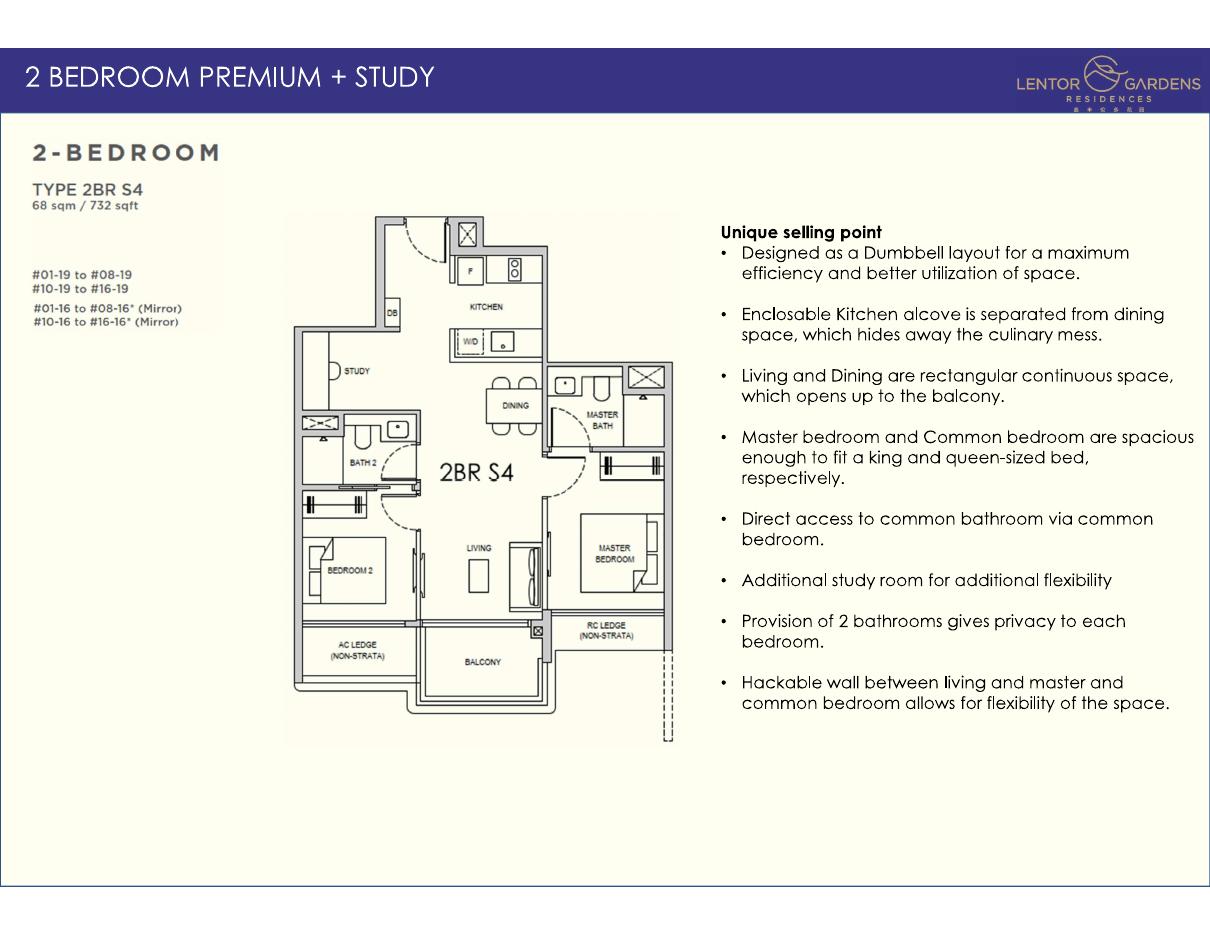

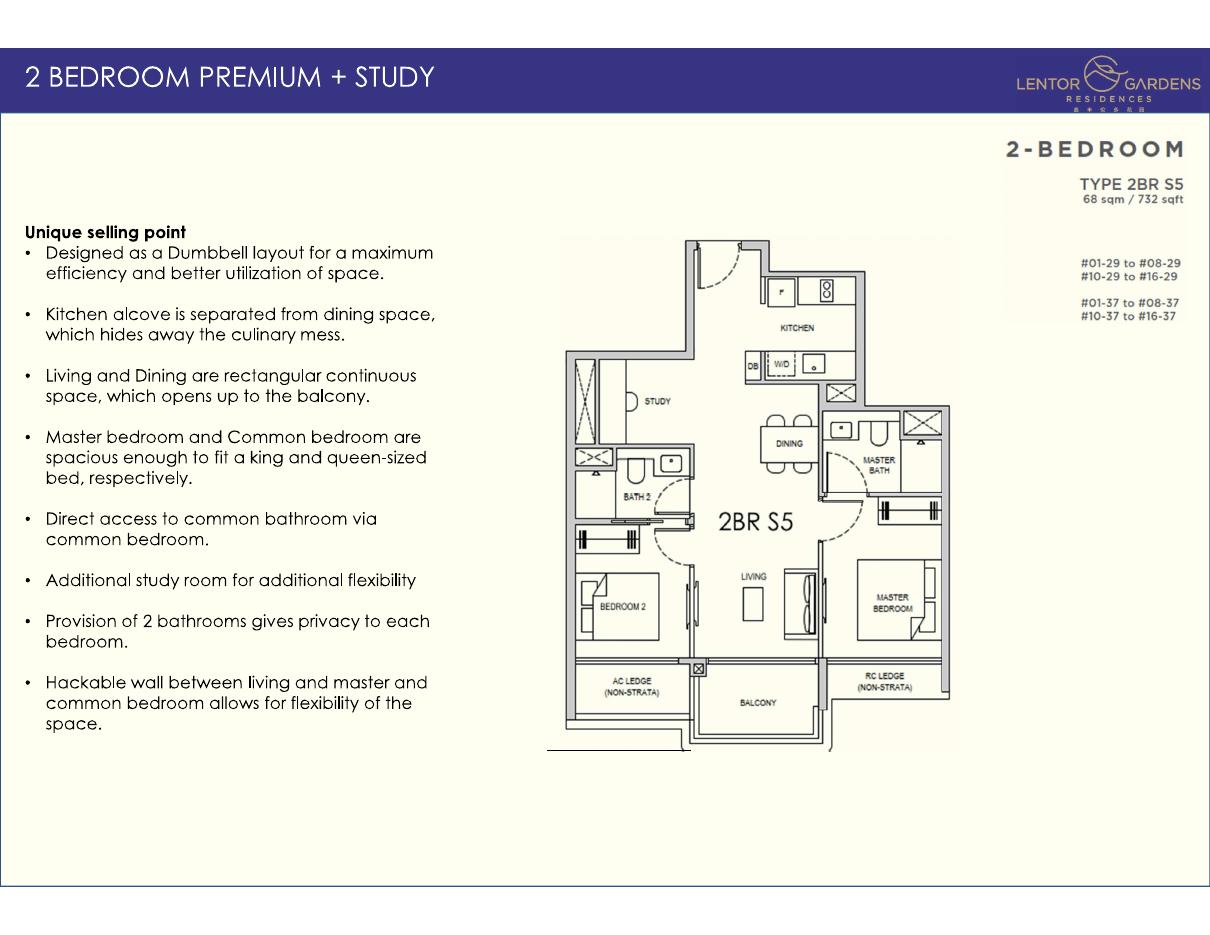

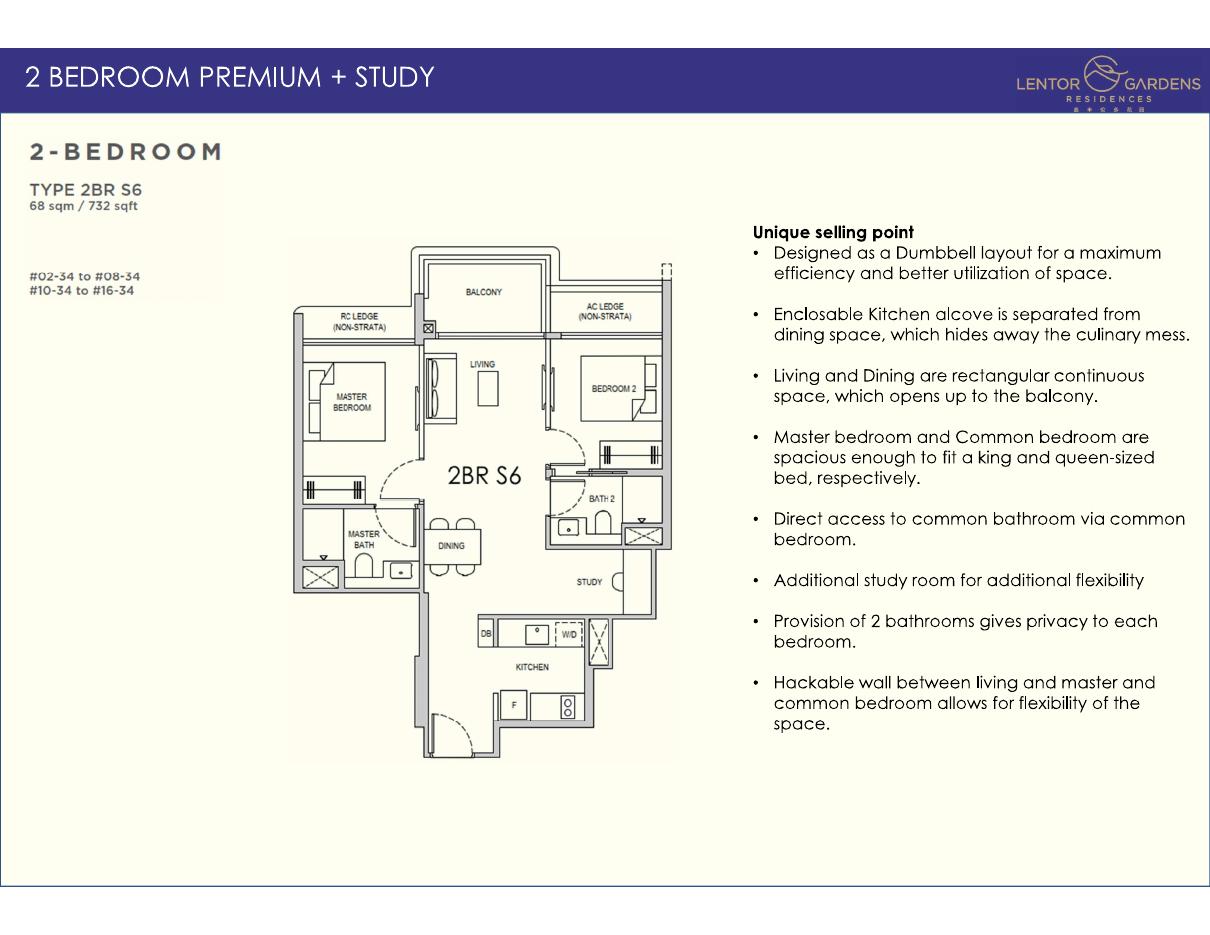

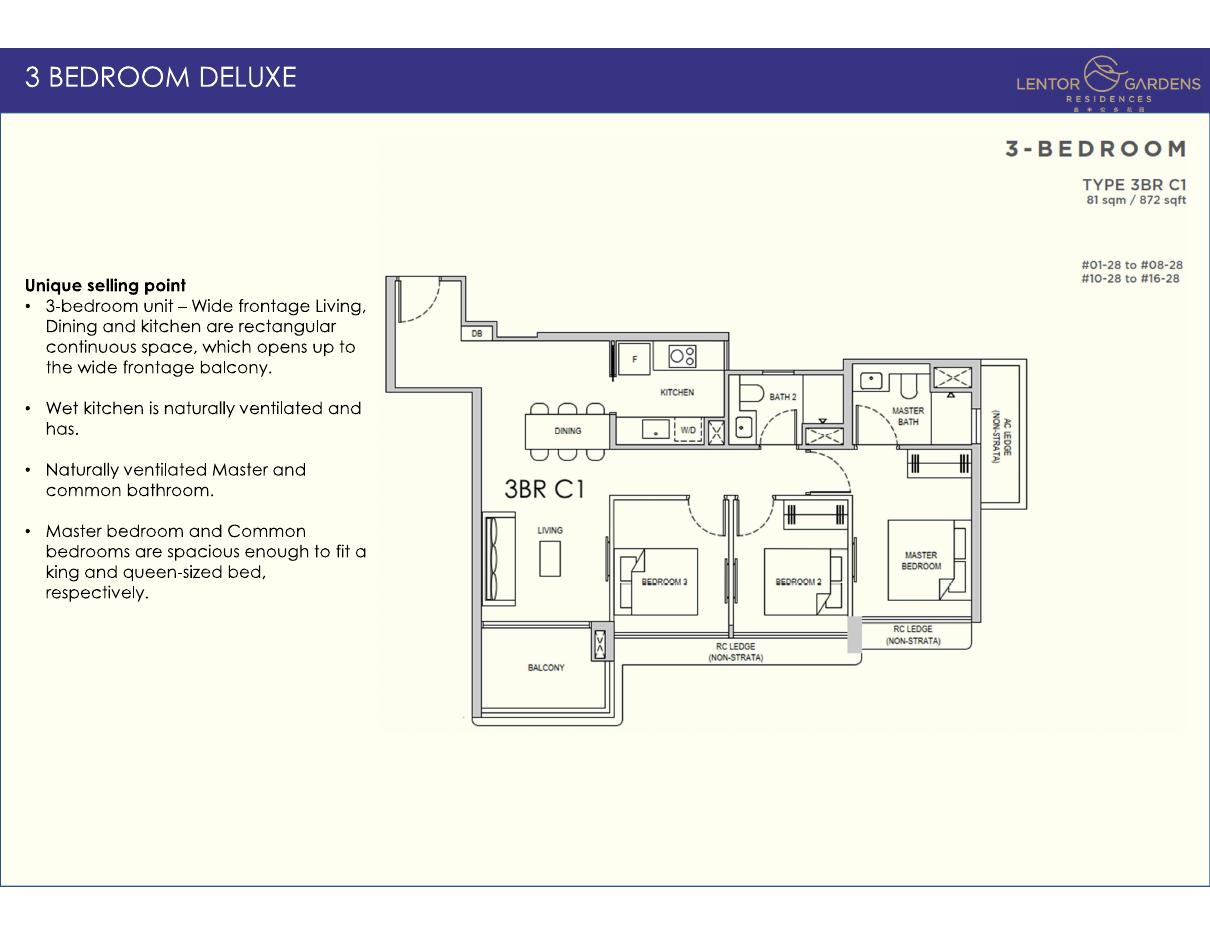

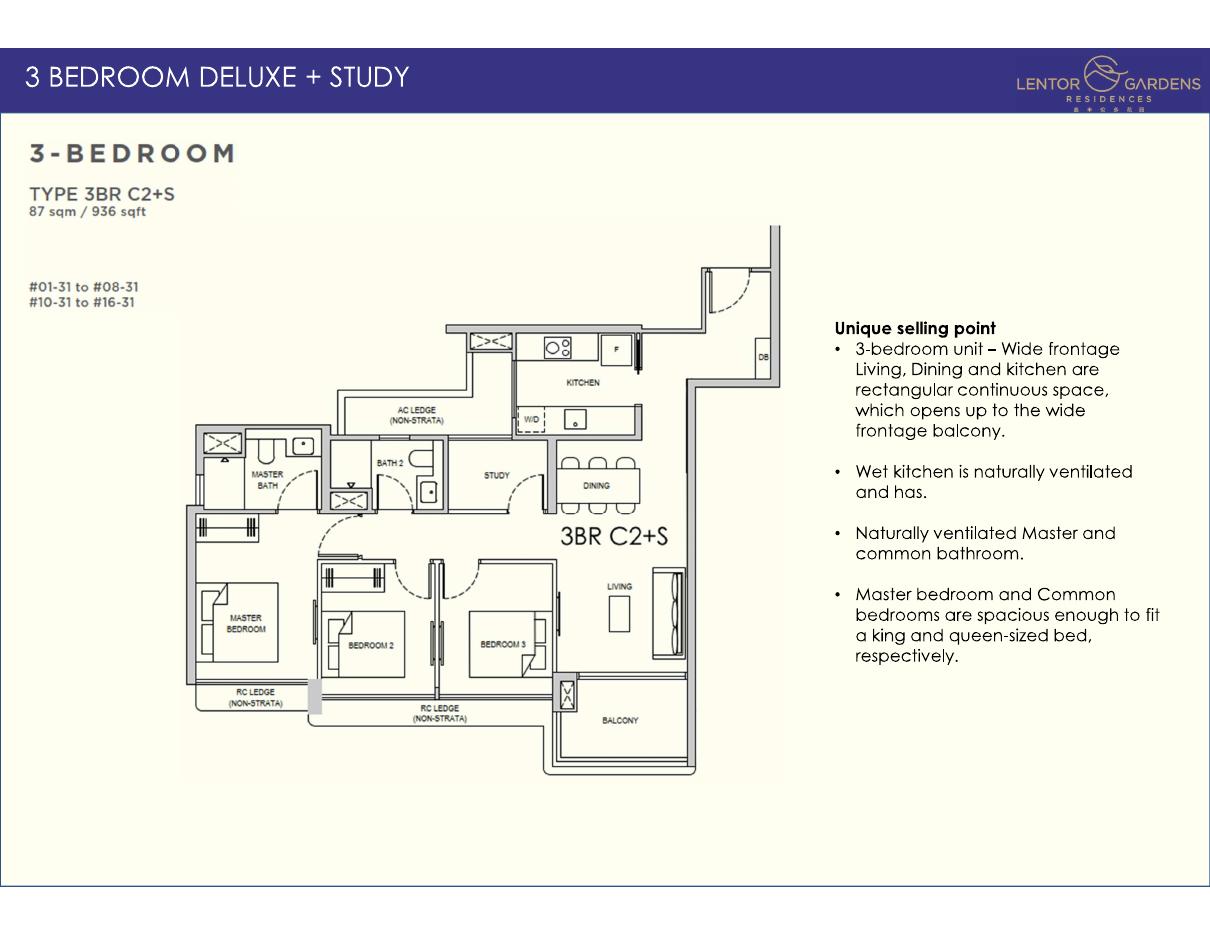

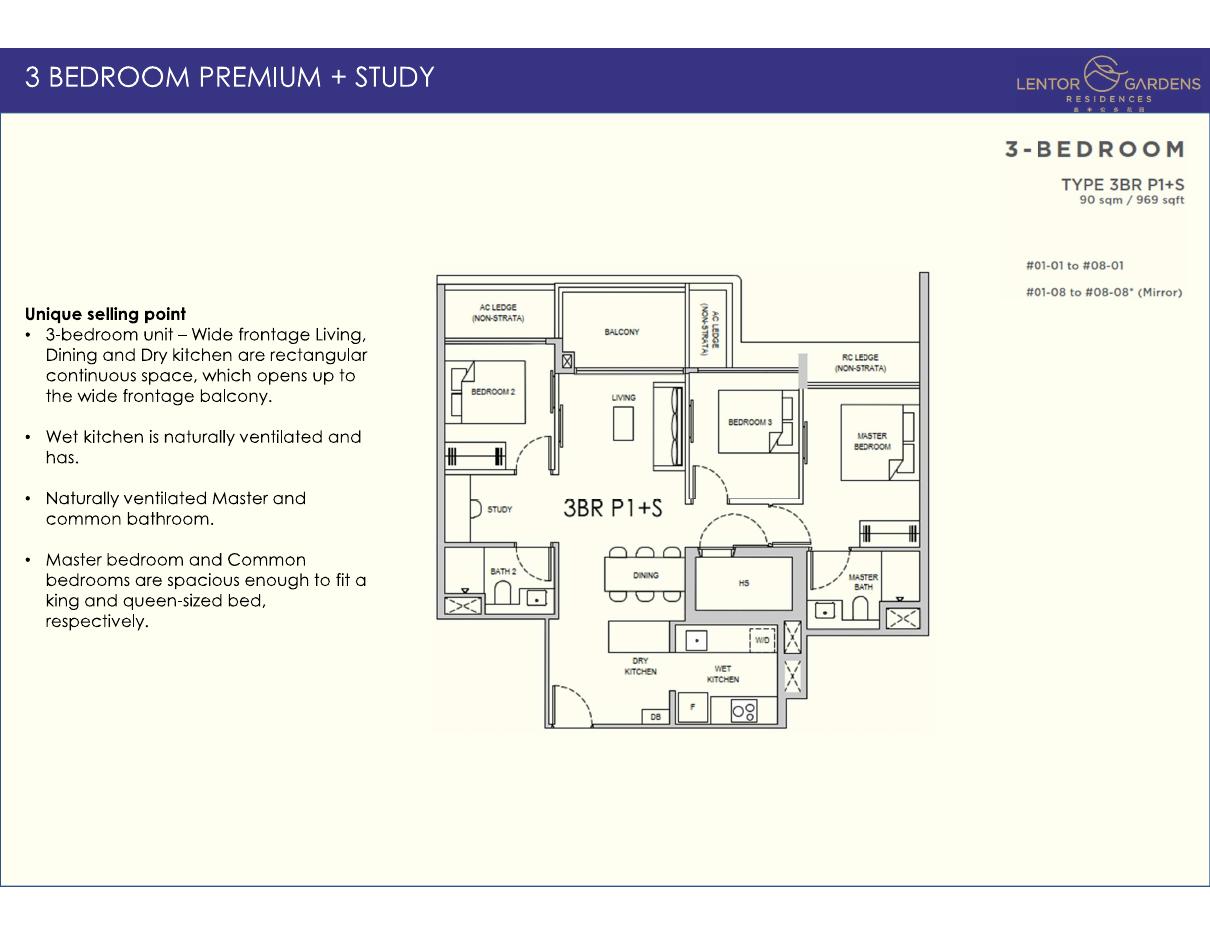

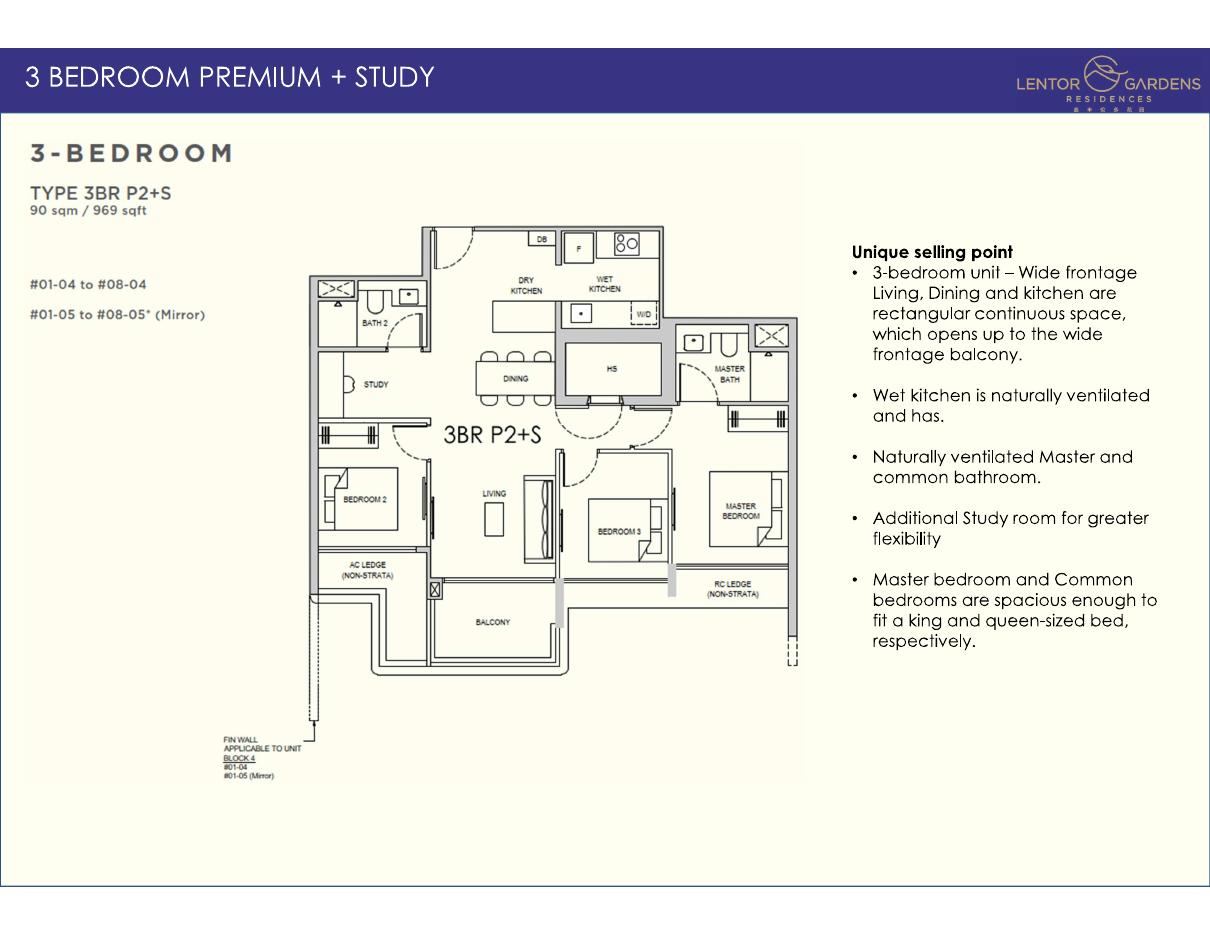

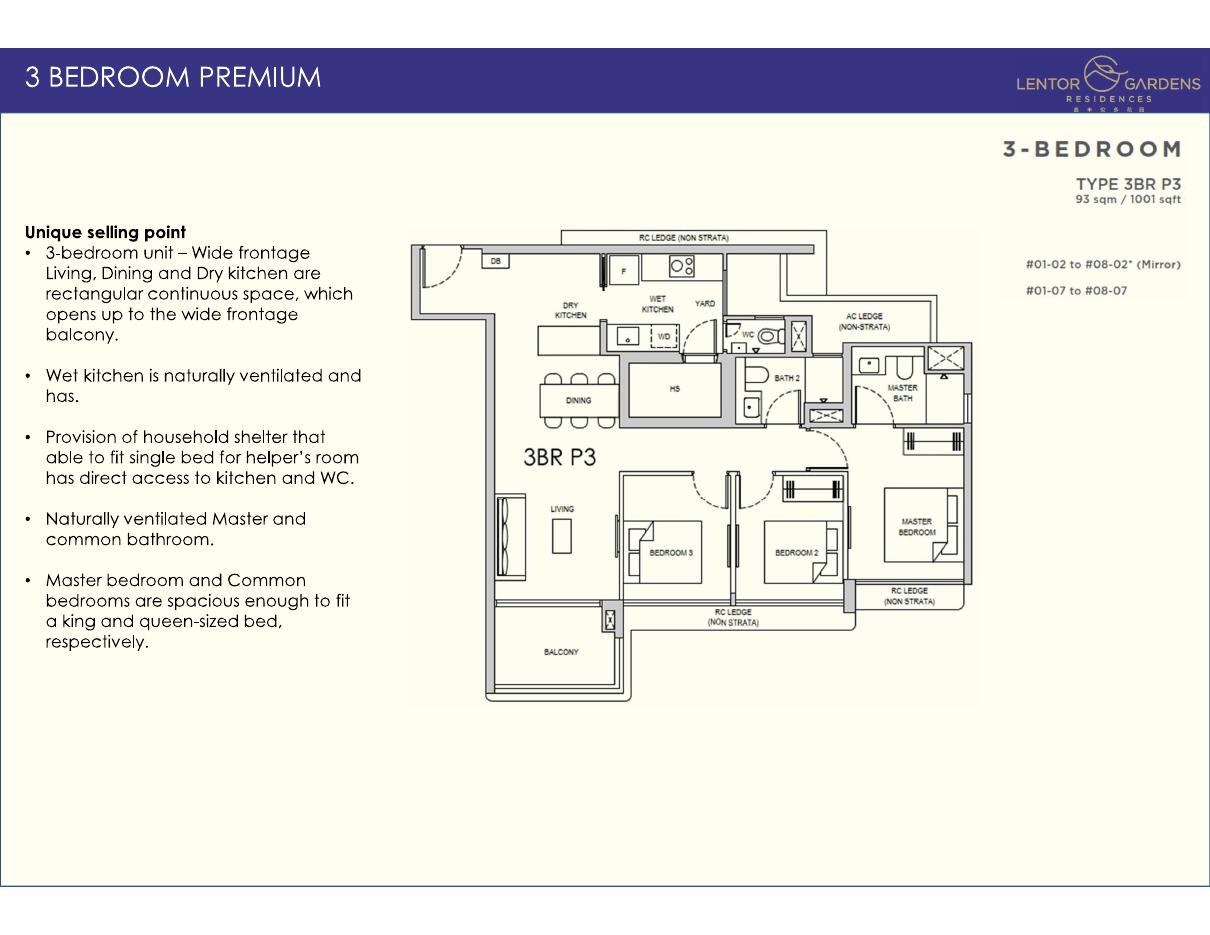

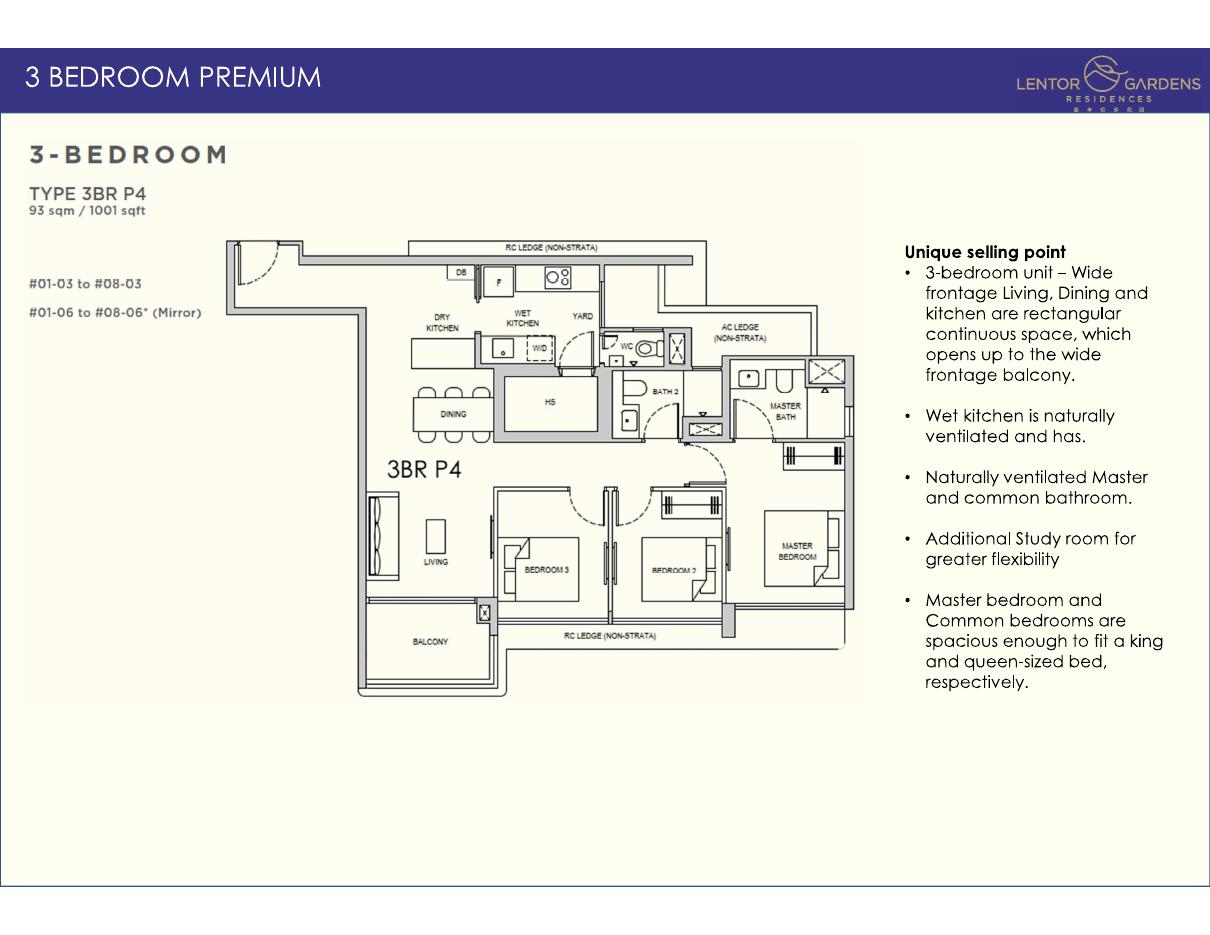

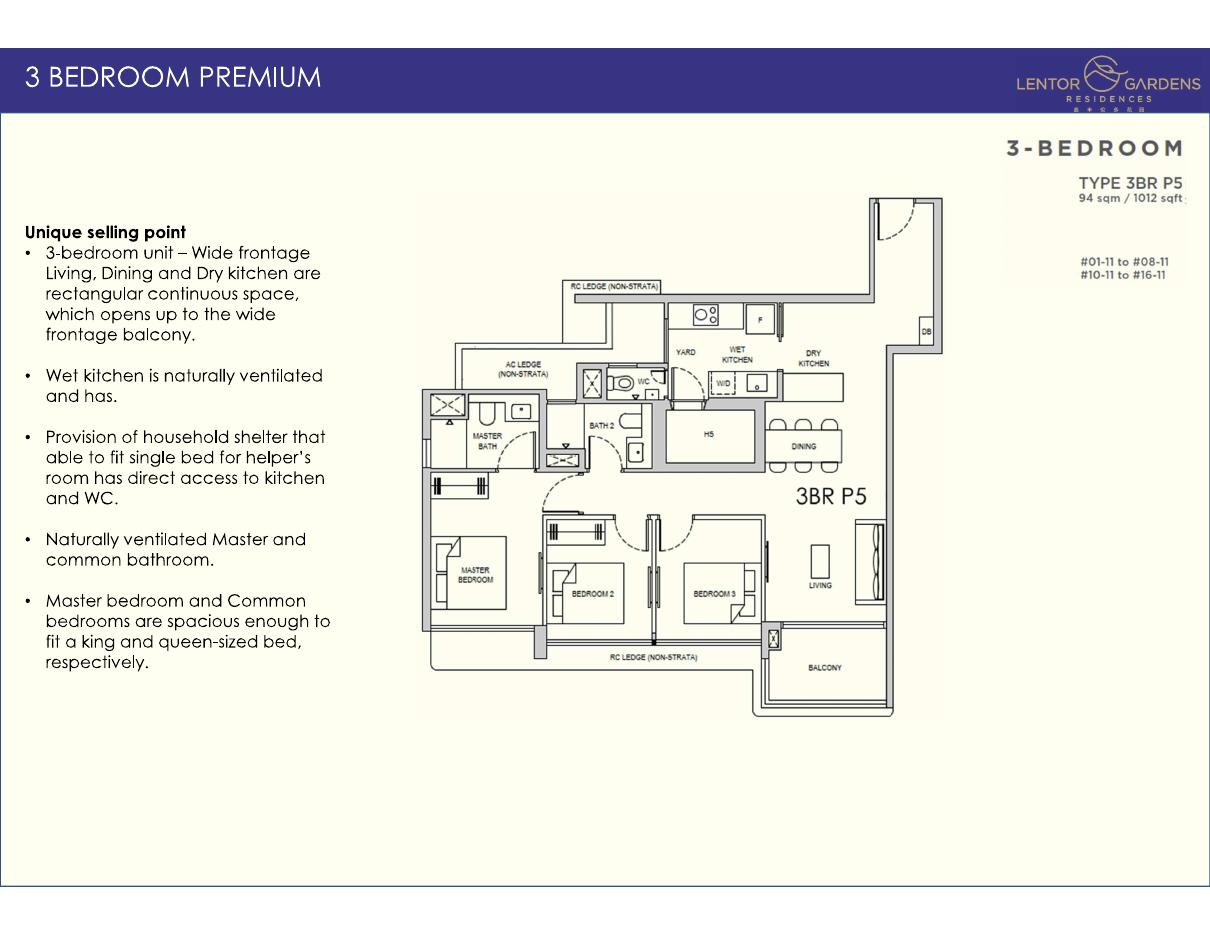

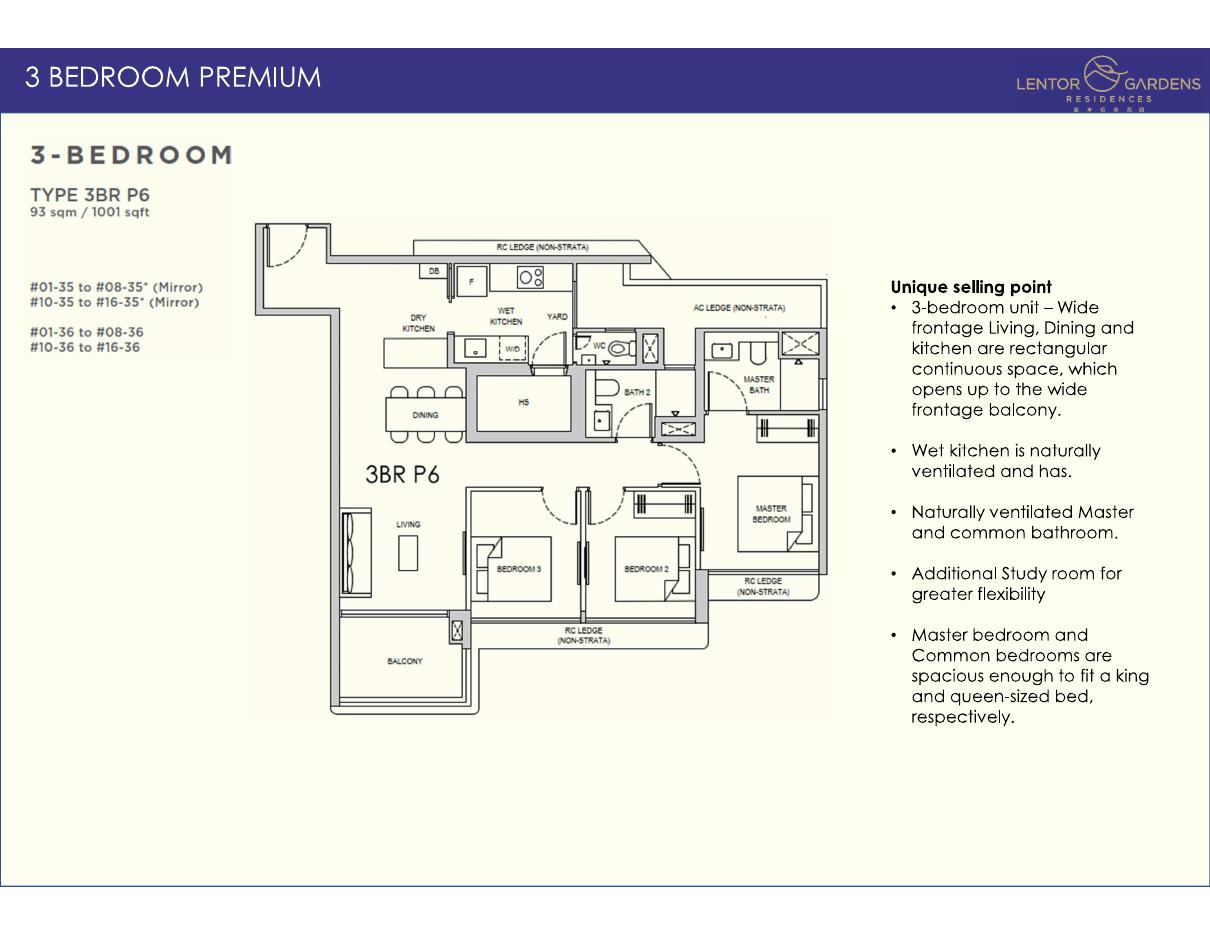

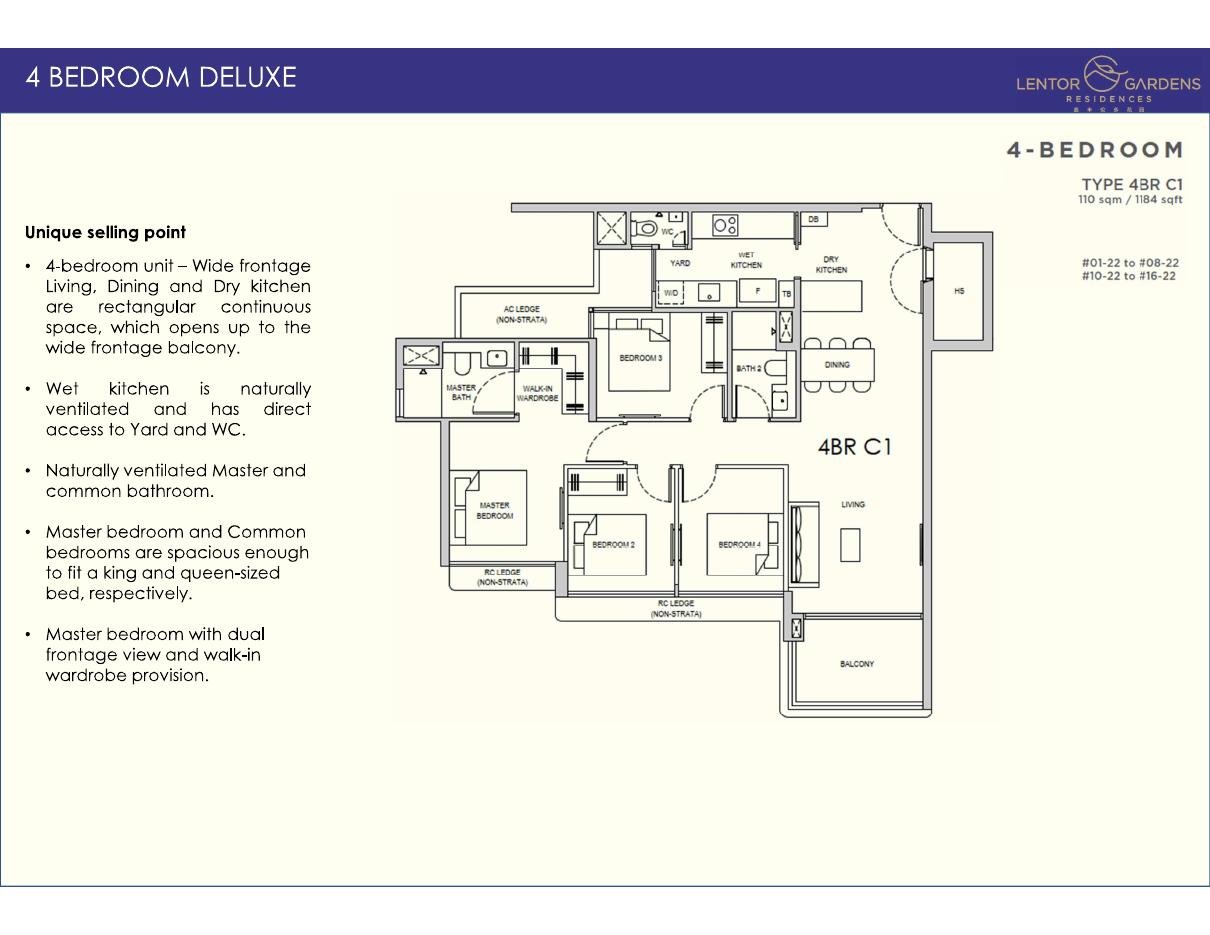

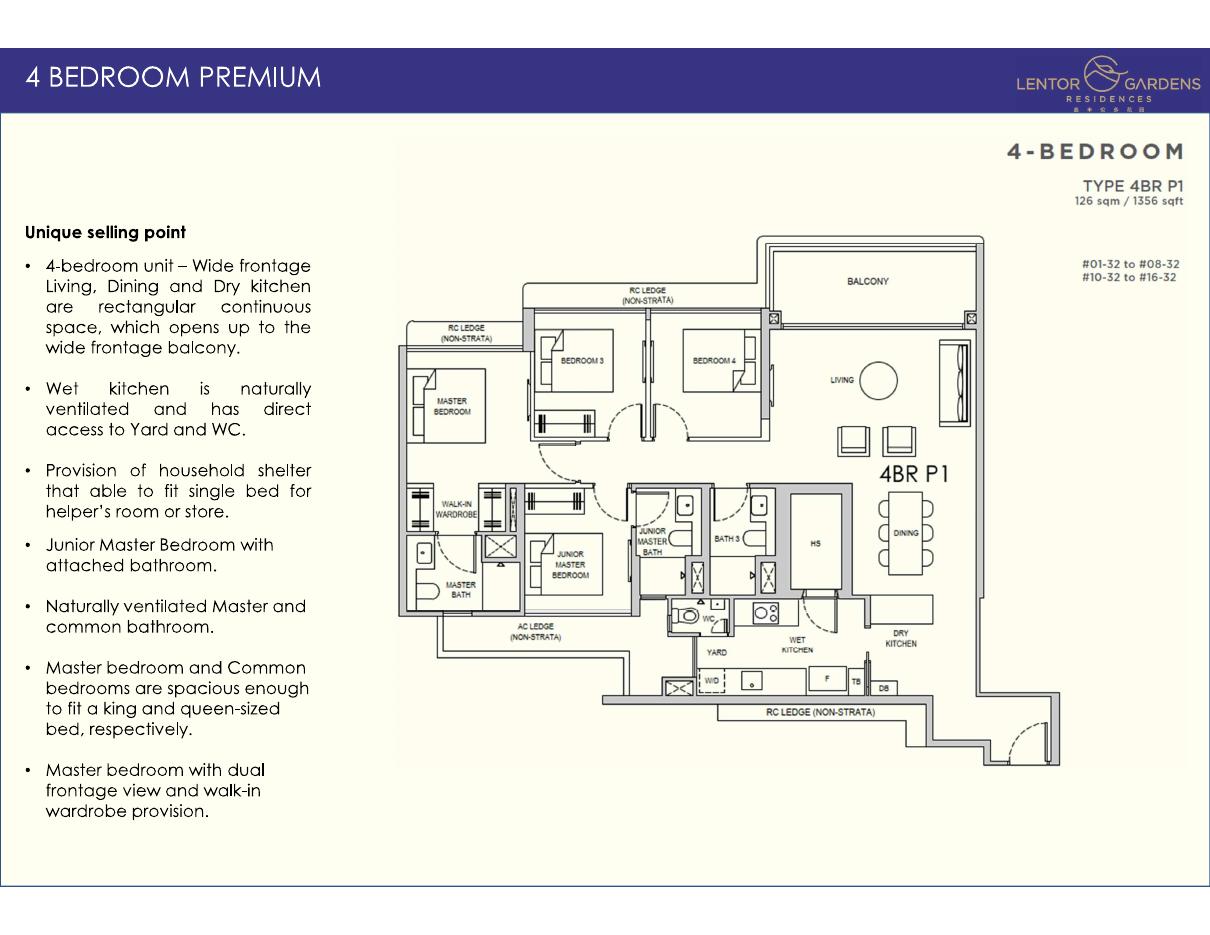

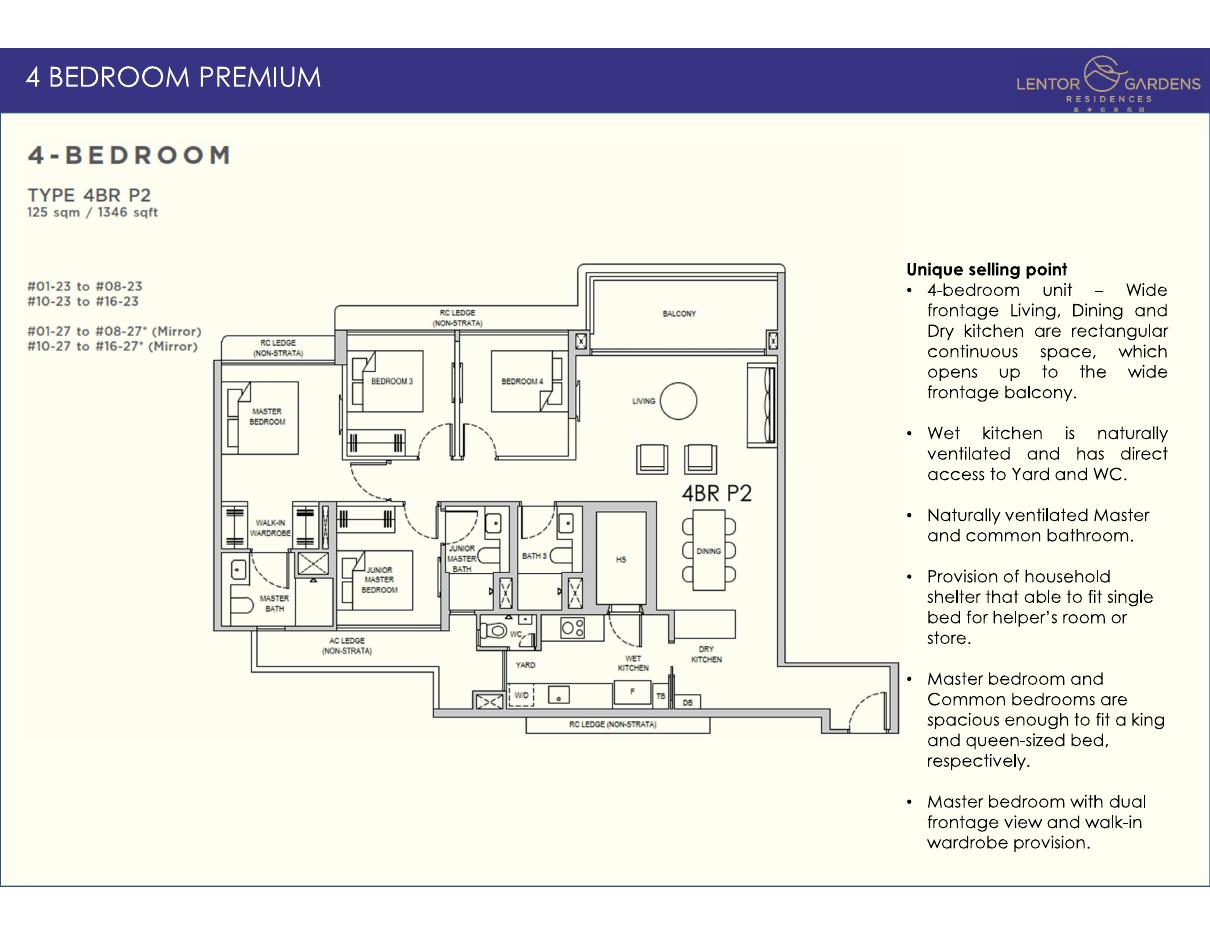

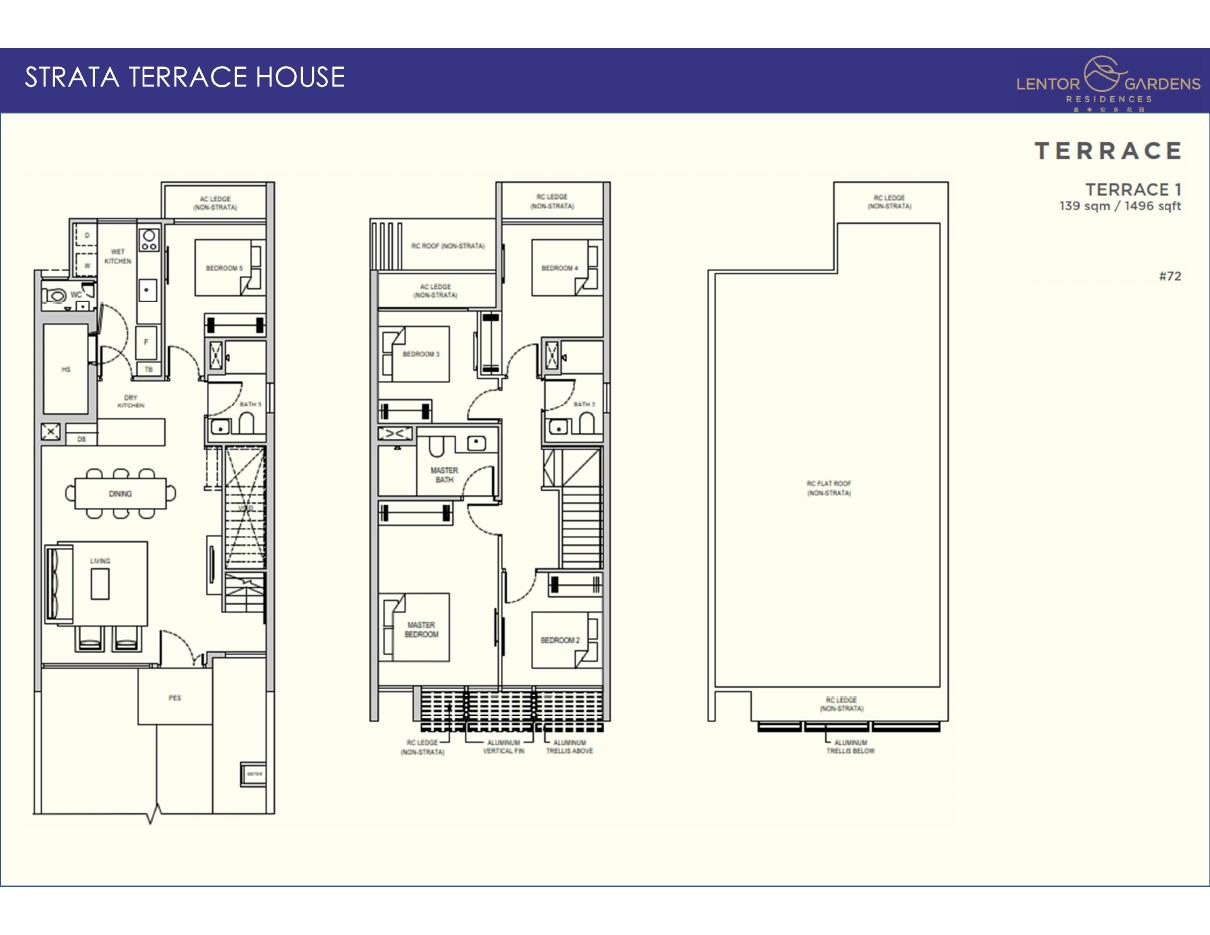

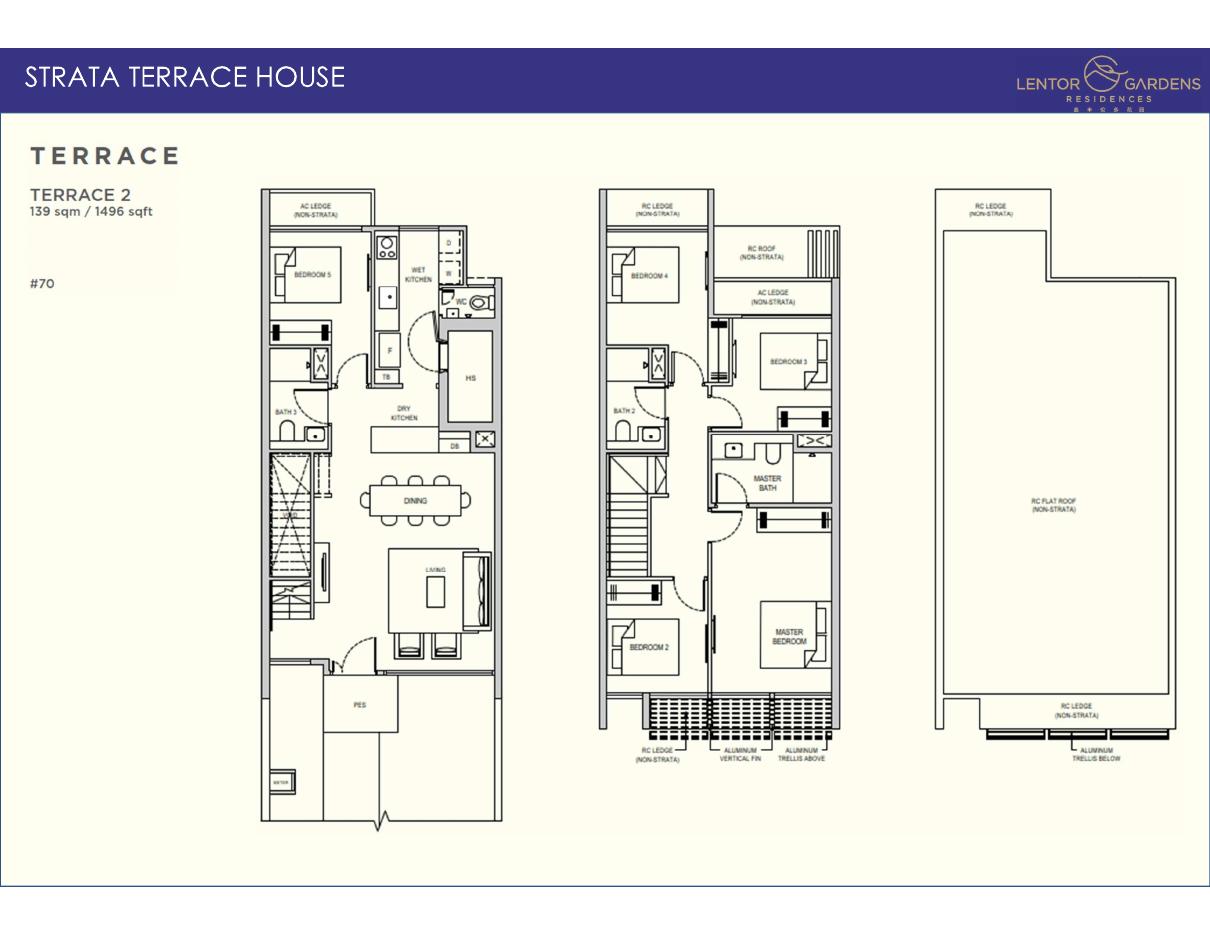

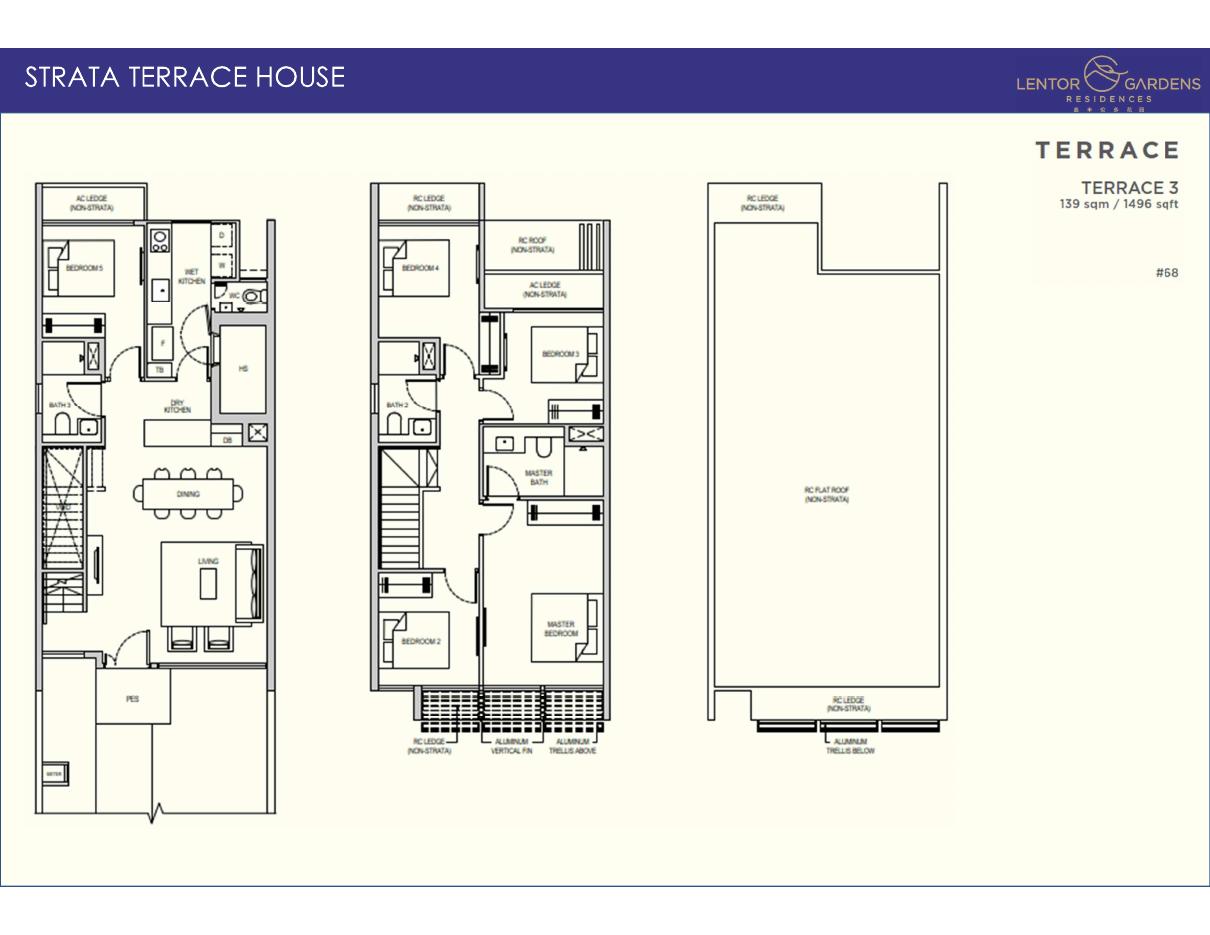

5. Site plan + floor plans

Start with the site plan, then browse the floor plans by unit type:

Floor Plans — browse by unit type

Site plan2 pages

2-Bedroom646–732 sqft · 252 units · 11 pages

3-Bedroom872–1,012 sqft · 139 units · 8 pages

4-Bedroom1,184–1,356 sqft · 105 units · 4 pages

Strata Terrace1,496 sqft · 3 units · 3 pages

Project architect briefing (P&T Consultants for Kingsford, May 2026) — site plan (deck pp 61, 63) plus all 26 floor-plan pages (pp 80–105).

6. Indicative pricing: no official list yet — the market's read, unit by unit

There is no developer price list. The briefing carries no pricing, and nothing official has been published anywhere haio can verify. What is circulating ahead of the 4 July preview is agent marketing material putting the entry at $2,050 psf and the size-weighted average around $2,350 psf — market indicative figures, unconfirmed, and not the developer's. They sit between the rails this article has already built — the §2 estimated breakeven (≈$1,582 psf) and the enclave's transacted band (§8, roughly $2,100–$2,400 psf) — nearer the top rail.

Until the real list drops, here is what those anchors imply for every one of the 499 units. haio distributed the two anchors across the project's actual stack map — each stack's facing, outlook and noise attributes from the briefing's site plan, a floor-by-floor lift, and the usual bedroom-type psf tiering — to give every unit a market indicative estimate. Filter by bedroom type; tap any unit:

Stack View — market indicative estimates

Market indicative estimates, not the developer's price list. Calibrated to the circulating anchors — entry $2,050 psf, ≈$2,350 psf average — distributed across all 499 units by stack, floor and bedroom type.

Blk 74 · Park row

Blk 74 · Pool row

Blk 76 · Park row

Blk 76 · Pool row

Blk 78 · Park row

Blk 78 · Pool row

Blk 66 · Pool-facing row

Blk 66 · Boundary row

Strata terraces (two-storey)

Market indicative estimates, not the developer's price list. Anchors: agent marketing flyer via Aaron, 2026-06-12 (msg 6515)— unconfirmed. Stack premiums are attribute-derived bands, not transaction-fitted; the developer's actual list can and will differ unit by unit.

Market indicative estimates, not the developer's price list: the anchors come from agent marketing material (12 June 2026), not from Kingsford; stack premiums are attribute-derived bands, not transaction-fitted; and the §2 land basis would allow the developer to open below these numbers. The moment the official list lands, haio will replace this model with the real per-stack read.

7. Affordability: what the likely quantum asks of you

No official prices exist, so this section runs on the §6 per-unit model — haio's market indicative estimates, not released prices — until the 4 July price list. Pick the unit you'd buy: the tool fills in its estimated price and size band, then flips the question — what does the same budget buy elsewhere, at each district's 12-month median transacted condo $ psf from haio's transaction records?

Instead of Buying — what the budget gets elsewhere

Instead of buying:

Est. price range: $1.59m – $1.93m (market indicative estimate)

…you can buy — condo units of the same size (646–732 sqft) actually transacted within that budget in the past 6 months, cheapest district median first:

Estimates only for the Lentor Gardens bands — market-indicative (the §6 stack model), not released prices. Alternative rows are real haio transaction records over the trailing 6 months (as at 2026-06-01): each district counts condo sales inside BOTH the selected type's size window and its price band (all sale types), and shows the median price of those matching units. Districts need 5+ matching sales to appear. The size window is an explicit filter from the Lentor Gardens unit grid — alternatives are matched on size, never labelled by bedroom: bedroom labels appear only when haio's matched unit records carry one (never inferred), and URA caveats stopped carrying unit numbers in 2022. Run your own income and rate numbers on haio's affordability tool.

These are haio estimates — the §6 per-unit model's quantum bands and median-psf-based size estimates. They are not released prices, and a launch below the anchors (which the §2 land basis allows) would pull every figure down.

In haio's affordability framing, a ~$1.6m entry quantum is the band where a dual-income couple comfortably inside the TDSR can transact a new 99-year-leasehold two-bedder beside an MRT station — versus the same money buying a larger but older resale unit further from the line. The three-bedders ask roughly what a landed-adjacent resale would in this part of the island; the four-bedders (outside the widget's four types) are a $2.4m-plus commitment that competes with older landed and large resale stock. The trade this launch asks a buyer to weigh is brand-new plus the TEL at walking distance against size-for-money elsewhere — and the four-plus years to 2030 vacant possession is part of the price. Run your own income and rate numbers on haio's affordability tool before the showflat does the maths for you.

8. Comparables: six neighbours and 2,715 caveats already frame the price

Lentor stopped being a frontier years ago. Since September 2022, six projects in the enclave have lodged 2,715 new-sale caveats, and their medians sit in a tight band.

The freshest prints sit higher. Over the last 12 months, Lentoria's new-sale median is $2,355 psf (38 caveats) and Hillock Green's is $2,231 (32 caveats). The most telling number in the enclave, though, is Lentor Modern: 32 sub-sales — first buyers reselling before the project is fully completed — at a median of $2,404 psf since October 2025. The enclave's earliest buyers are already exiting roughly $300 psf above the project's $2,103 new-sale median. And in the wider District 26 corridor, Springleaf Residence has lodged 697 new-sale caveats at a median of $2,173 psf since August 2025 — proof the demand pool extends beyond the enclave itself.

Source: URA caveat data, haio transaction records (12-month window to 12 June 2026; Springleaf Residence: Aug 2025 – May 2026).

Comparable Projects — median $ psf, 12 months

haio transaction records (URA caveats) — per-project median $ psf across all sale types, 12 months to 12 Jun 2026. Lentor Hills Residences (n=2) and Lentor Central Residences (n=5) are thin counts — read those bars as indicative only.

Put §2 and §8 together and the launch maths writes itself: the band Kingsford must sell into is roughly $2,100–$2,260 on launch medians, with the freshest prints pushing $2,350–$2,400 — while its land cost sits $62–284 psf ppr below every parcel awarded in the estate's 2021–2023 tender run — the parcels those neighbours rose from. No other Lentor launch has opened with that spread.

haio's take

The product is unusually coherent: the missing one-bedders, two baths in every two-bedder, household shelters, hackable walls, childcare downstairs — every decision points at the same owner-occupier buyer. And the economics are unusually visible: the cheapest land in the estate's history ($920 psf ppr, verified against URA records), an estimated breakeven around $1,582 psf, and a developer whose pattern — Normanton Park, Chuan Park — is to price for year-one volume. If the 4 July price list lands under the enclave band, the no-shoebox bet stops being brave and becomes the obvious family buy in Lentor, and the land-cost advantage is being passed to you. If it opens at the top of the band, Kingsford is keeping the spread — and you're paying the family premium plus four years of waiting for it. Watch the first price list, not the showflat queue.